The head of the Financial Technology Association defended buy now, pay later (BNPL) financing deals at a congressional hearing last week against claims by critics that they encourage consumers to spend more than they can afford, damaging their credit score in the process.

In testimony presented to the House Financial Services Committee's Task Force on Financial Technology, Financial Technology Association CEO Penny Lee argued that BNPL services offer consumers a better deal than credit cards that charge high-interest rates that can take years to pay off. She said that technological advances like BNPL also lower borrowers' costs and increase choice for both consumers and businesses.

"There is a shift in how millennials, Gen Zers, and others are spending their money," Lee said. "They are saving more and utilizing credit cards less, preferring debit cards with no fees or revolving interest rates."

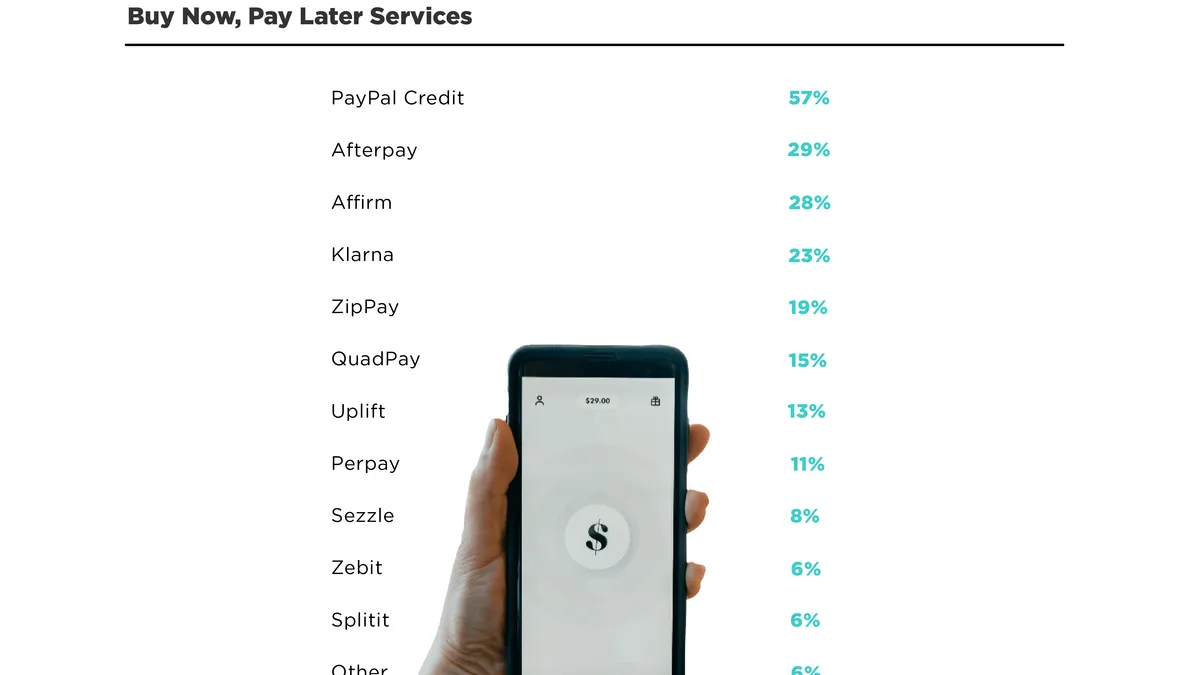

BNPL allows consumers to finance purchases by spreading out payments, which are typically interest-free, over a short period over six to eight-week period.

At the same time, the U.S. market is still in its infancy compared with other parts of the world though demand for BNPL continues to soar, the coronavirus pandemic notwithstanding.

Accenture estimates that BNPL spending increased 230% since the start of 2020. BNPL will account for 6% of U.S. e-commerce sales in 2021, or $974.2 billion. By 2025, that figure will top $1.4 billion, or 13% of online shopping, according to Accenture.

Critics have many concerns.

"As we saw with credit cards being pushed on college campuses, this can saddle young people with debt, starting their journey to adulthood with damaged credit and potential for life-long negative financial consequences," said Marisabel Torres, director of California policy at the Center for Responsible Lending, in testimony before the House. "There is also concern that the entire business model of buy now-pay later rests on driving borrowers to purchase items they would not otherwise buy."

According to a Credit Karma study, 34% of BNPL users have fallen behind on one or more payments. The survey found that 72% of users said they believe their credit score declined. More than 30% of respondents said their credit score decreased significantly.

Lee countered the argument by critics, noting that 97% of BNPL users didn't incur late fees.

"The benefits of BNPL are apparent regardless of merchant size, with large and small merchants seeing considerable improvement across business metrics," Lee said. "Another recent survey found that merchants using a particular BNPL solution enjoyed 13% more new customers."

Credit Karma also found 44% of Americans used BNPL to buy products they needed, up slightly from a year earlier. Three-quarters of BNPL users have tapped the service at least twice, according to Credit Karma.

"The exponential growth of these alternative financial products clearly shows that consumers want them," said Rep. Warren Davidson (R-OH). "We should avoid punishing new products, not fitting within regulatory buckets that were already built," Davidson said during the hearing. "You should avoid overly impairing consumer choices on how they spend money, and we should facilitate innovation."