The payments space is experiencing a lot of change.The pandemic's influence over how retailers and consumers think about payment channels is still present today.

The buy now, pay later model has been on the rise, and with it, concerns over consumer debt levels as more shoppers take on payment plans for everyday purchases. The advantages of checkout-free capabilities are still being tested, as retailers pursue convenience in new store concepts. And retail giants like Walmart and Amazon are introducing new payment offerings and pursuing deeper efforts in the space as consumers' preferred payment options change.

But, most of all, it feels like retailers are thinking through the best way to streamline and incorporate payment options as a way to capture, delight and retain shoppers. As the space shifts, the future of who will best utilize and employ new means of supporting retail operations through different payments is anyone's for the taking.

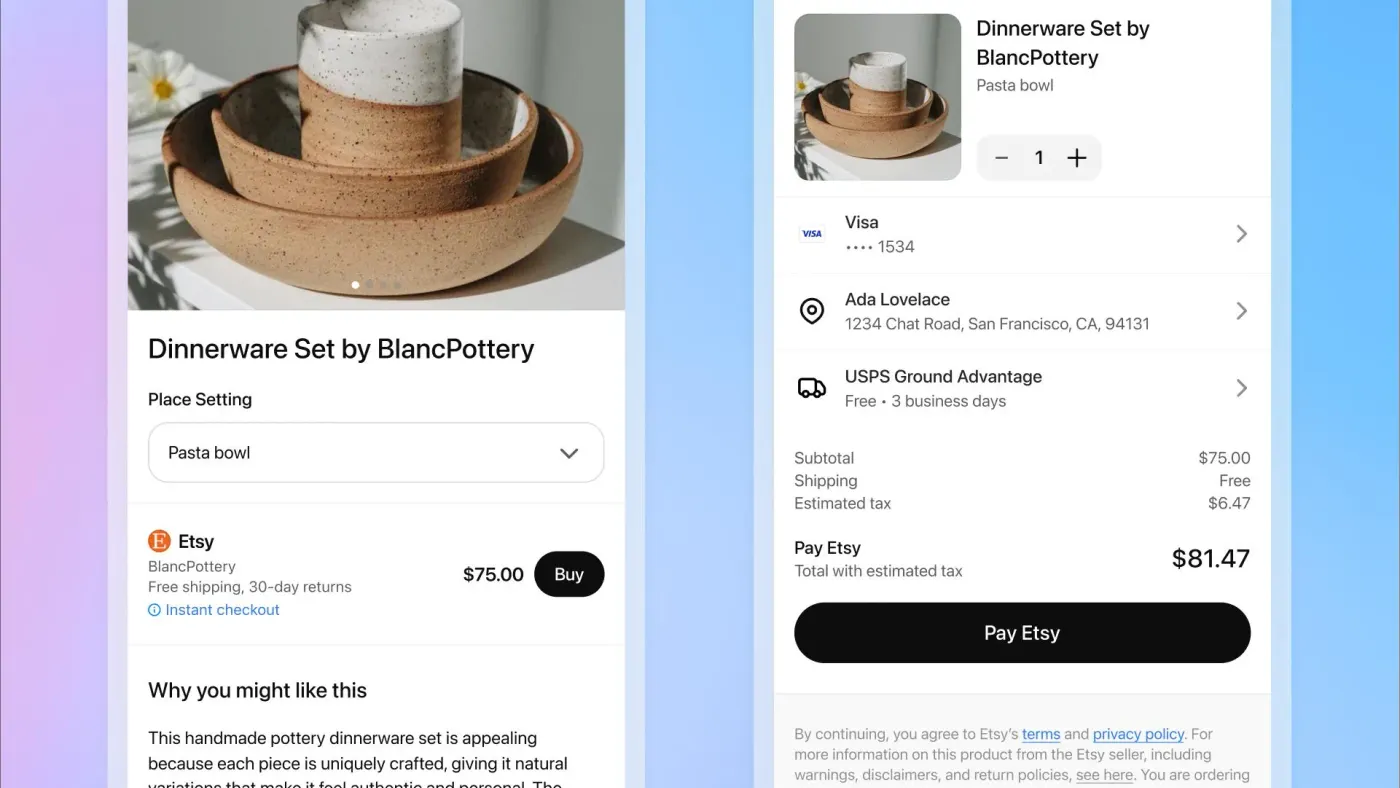

ChatGPT lets shoppers buy products within the platform

Launching first in partnership with Etsy and Shopify, the Instant Checkout functionality has the potential to rival Amazon and Google, one expert said.

By: Dani James• Published Sept. 30, 2025

As consumers turn to AI for shopping recommendations, OpenAI just announced a function that aims to keep the buying process on its ChatGPT platform.

The company in September debuted Instant Checkout for U.S. ChatGPT Plus, Pro and Free users. Such users can now buy directly in the platform from U.S. Etsy sellers and will soon have the same option for over a million Shopify merchants (including Glossier, Skims, Spanx and Vuori).

"As a marketplace of over 5 million creative entrepreneurs, it’s our job to remove barriers for shoppers so they can easily discover and be delighted by our sellers’ special items," Etsy Chief Product and Technology Officer Rafe Colburn said in a separate company post.

The Instant Checkout functionality currently supports single-item purchases, but OpenAI plans to add multi-item carts as an option and expand the service to additional regions.

Merchants pay a fee on purchases, though the service does not come at an additional cost to ChatGPT users, and items with Instant Checkout are not preferred in product results, per OpenAI. However, the tech company said in its announcement that it does consider several factors — such as the enablement of Instant Checkout, quality and price — when ranking merchants that sell the same product.

The new feature is powered by the Agentic Commerce Protocol, which the technology company says was built with Stripe and other partners. In addition to this initial Instant Checkout rollout, OpenAI has open-sourced its Agenetic Commerce Protocol for merchants to start building their own integrations. Businesses can then apply to have their products available to buy through ChatGPT.

"OpenAI is taking its first big step into commerce with Instant Checkout,” Emarketer senior analyst Zak Stambor said in emailed comments. “The feature still has some wrinkles to iron out, but embedding checkout for hundreds of millions of users could turn ChatGPT into a true commerce destination. If OpenAI can streamline the experience, it could challenge Amazon and Google and carve out a lucrative new revenue stream."

The news from OpenAI comes as shoppers turn to AI to ask for product suggestions on anything from everyday essentials to holiday gifts. The impact means that some consumers are shifting away from the search engines retailers have long focused on and changing the nature of their searches to be more complex, even directly on a company’s e-commerce site.

GEO, or generative engine optimization, is the future of SEO, Target’s Vice President of Digital Product Management Ranjeet Bhosale told an audience at ShopTalk Fall 2025 in September.

“It’s not just about giving them the right products. It’s also about how you showcase the product,” Bhosale said. “When they are searching for a summer party, rather than just showcasing tableware they are expecting us to now show party supplies, grilled meat, even sunscreen, and show the breadth of assortment that Target carries in a meaningful fashion.”

Article top image credit: Retrieved from Etsy on September 30, 2025

Checkout-free payments may yet rise

Advancing artificial intelligence could let cashierless payment companies succeed where Grabango failed, industry insiders and observers say.

However, that progressive, lower-cost, digital approach to in-store retail payments isn’t dead. A technological boost could still help checkout-free payments succeed, say industry professionals and consultants.

“I still believe there's huge opportunity in this space,” Ken Fenyo, who was Grabango’s chief marketing officer, said in an interview in May. “Artificial intelligence will help companies put together the kind of solution that the market needs.”

Even with the rise of e-commerce, the majority of shopping still happens in-person. U.S. consumers spent $5.93 trillion in retail stores in 2024, according to research from Capital One published in May, compared to $1.34 trillion online. Retailers operate on thin profit margins and are constantly looking to trim costs and checkout-free technology offers the enticing prospect of accepting a customer’s money without paying a cashier.

Multiple companies, including San Francisco-based Zippin and Malvern, Pennsylvania-based Cantaloupe Technologies, offer checkout-free systems for retailers and venues such as stadiums.

Patrick Cooley/Payments Dive

“At the most basic level, there’s always going to be an appetite for a checkout-free process,” said Tony DeSanctis, senior director of payments for the consulting firm Cornerstone Advisors.

A checkout-free system tracks a customer’s movements while he or she is shopping and automatically records their selections when they pull items off the shelf. The system uses cameras to track shopper activity in concert with shelf sensors that sense when items are picked up. Increasingly, the systems rely on artificial intelligence to recognize customer selections.

Checkout-free payments are most appealing in settings where a large number of customers want to make purchases quickly, said Krishna Motukuri, CEO and co-founder of Zippin, a San Francisco-based checkout-free payment company that has raised $37 million in equity investments. One such setting is a stadium or a sports arena, where the games have regular breaks that result in mass trips to the concession stand, he said.

Patrick Cooley/Payments Dive

“That creates a bit of challenge where some people never line up [because they see a long line], and that ends up being lost revenue,” Motukuri said. If customers can purchase faster, “more people are willing to shop and that revenue comes back in.”

The fan experience is top of mind for stadium operators that use checkout-free concession stands, said Adam Nuse, senior vice president for the Tennessee Titans. The Titans play in Nashville’s Nissan Stadium, which has checkout-free concessions.

“Shorter lines mean more time at your seat enjoying the game,” he said in an emailed statement.

The role of artificial intelligence

The technology tends to struggle with bulk-price items in a supermarket setting, like tomatoes or mushrooms. Grocery stores often charge for fruits and vegetables by weight rather than per item, which makes pricing produce an arduous task for a camera tracking system. But AI, which is advancing at an astonishing pace, will eventually improve that process.

Burlingame, California-based AiFi is already using artificial intelligence to help stores eliminate the checkout. AiFi’s cashierless system is in 300 stores globally, CEO Steve Carlin said in an interview, and it counts companies like Aldi, Dollar General and The Compass Group as customers.

“AI is first tracking a body,” he said. “The system then looks for what we call ‘activities of interest:’ When people shop for things, they stick a hand out into space, grab something and pull it back.”

If a customer reaches for a bottle of Coca-Cola, and then there is one less bottle of Coca-Cola on the shelf, the system will charge the customer for that soda bottle, Carlin said. He contended that AiFi’s system is more than 99% accurate and has advanced enough to be used in any store or supermarket.

Lori’s Gifts, a chain of gift shops with around 400 locations mostly in hospitals, uses AiFi’s system to keep its shops open around the clock, said Brandon Glenn, the company’s vice president of marketing.

“We can meet the growing demand for 24/7 access without the need [for customers] to wait in line, or rely on traditional staffing,” he said.

History of checkout free shopping

Checkout-free payments evolved from self-checkout kiosks.

Store owners used the kiosks to cut labor costs, said John Talbott, a professor of marketing at the Indiana University Kelley School of Business who studies retail.

“Convenience stores are labor-intensive,” he said. “And it’s difficult to find people to reliably work the shifts, because they often are open 24 hours.” Stores have trouble hiring workers for the night shift, or who are willing to stay in a position that requires overnight work, Talbott said.

An earlier version of cashierless checkout, the ubiquitous self-checkout line, has proven troublesome. Research shows self-checkout is an inviting target for shoplifters, raising questions about whether or not it is worth the savings, DeSanctis said.

Enter checkout-free shopping, which carries with it the cost savings of a self-checkout with less opportunity for theft.

The first store to offer cashierless payments was an Amazon Go store in Seattle that used the company’s “Just Walk Out” system and opened to the public in 2018, Talbott said.

Grabango — which was founded in 2016 — officially launched its first checkout-free system at a GetGo convenience store near Pittsburgh in 2020. Then, in a test of a broader market audience, grocery chain Aldi opened a checkout-free store in the Chicago suburb of Aurora using Grabango’s technology in early 2024.

Why Grabango failed and Amazon pulled back

San Francisco-based Grabango wasn’t adding locations fast enough to impress potential investors and secure a needed funding round, said Fenyo, who is now an independent consultant.

Not enough retailers were ready to widely use checkout-free systems, Fenyo, said. “They were testing it slowly, rolling it out. But it wasn't at the pace venture capitalists wanted.”

Store customers’ gradual acceptance of Grabango technology is part of what gives Fenyo the confidence that there will eventually be a strong market for checkout-free shopping.

Grabango’s research found shoppers were initially repelled by the technology, but started to prefer checkout-free payments once they use them a few times, he said.

“We had stores with Aldi, and Circle K, and I think we were seeing adoption,” Fenyo said.

When Amazon announced in 2024 that it was removing checkout-free technology from its U.S. supermarkets, a company spokesperson told CNBC that customers liked the system, but preferred shopping for deals and checking their receipts as they browsed the store.

Amazon's system also had another major flaw, Talbott said. It made returns and customer disputes more complicated since there were fewer employees in the store.

Additionally, the company's Just Walk Out was questioned in 2024 after a reports said the technology relied on hundreds of workers in India. Amazon responded in a blog post, stating that the reports were "erroneous" and that associates don't watch live video of shoppers to generate receipts, but that those processes were taken care of automatically by computer vision algorithms.

However, even as Amazon removed checkout-free systems from its own stores, it continued to sell the technology to third parties such as stadiums, hospitals and college campuses. The Seattle-based e-commerce giant revealed in 2024 that it was installing a checkout-free system at St. Joseph’s/Candler hospital system in Savannah, Georgia, making it the first hospital to use the technology. A St. Joseph’s/Chandler spokesperson did not respond to a request for comment.

Why checkout-free technology can still work

Artificial intelligence will help companies put checkout-free systems in more stores, Fenyo predicted. “I think you're going to see that over the next few years it will begin to emerge and rapidly scale up,” he said.

As AI improves, it will make checkout-free systems more accurate and efficient, and able to identify more items, expanding the number of stores that can use checkout-free technology, Fenyo said.

“It’s hard to see what retail formats would work in a way that 100% of the items would lend themselves to this technology,” Bowman said. “And product assortments always change.”

But as artificial intelligence improves, it will reach the point that a checkout-free shopping system can recognize more opaque items, Fenyo said.

“We were close [at Grabango], but not quite where we needed to be,” he said.

The costs are also coming down, Motukuri said. And as expenses continue to fall, “you’ll start to see more of these stores around the country.”

And not everyone is convinced it can work.“I've always wondered if it was a solution looking for a problem,” said Douglas Bowman, a marketing professor at Emory University’s Goizueta Business Schoolwho studies consumer behavior.

Cutting costs is appealing to merchants, but consumers aren’t clamoring for the technology, he said.

“If Amazon can't do it, I don't know that anybody can,” Talbott said. That company is “extremely capable from a tech standpoint” and has “infinite amounts of money to spend.”

Major grocery chains and retailers either did not respond to a request for comment or declined to discuss their use — or avoidance — of checkout-free systems.

A spokesperson for Giant Food declined to comment while spokespeople for Walmart and Kroger did not respond to requests for comment.

Article top image credit: Permission granted by Lori's Gifts

Klarna counts on retailers for growth

The buy now, pay later giant says the availability of its services at retailers such as Walmart and Macy’s correlates strongly to future growth.

By: Justin Bachman• Published Sept. 11, 2025

Klarna Group wants to make its buy now, pay later option "ubiquitous" at the retail checkout as a primary engine for future growth, the company’s chief commercial officer said in September.

“Our aspiration is to be ubiquitous at the checkout, and what that drives is actually a habitual behavior of, ‘I see Klarna, it's regular, I can use it more often,’” Chief Commercial Officer David Sykes said in an interview a day before the company’s initial public stock offering.

One area of retail progress: Klarna will debut its short-term loans at Walmart in September, a company spokesperson said. That lending debut comes six months after the company announced that it had wrested the largest U.S. retailer away from BNPL rival Affirm Holdings.

Klarna is being incorporated into Walmart’s OnePay digital payments app that shoppers can use at their checkout in stores and online. Loan repayments will range up to three years, managed via the OnePay app, the companies said in March announcing their partnership.

Klarna’s business began in Sweden, spread across Europe and has spurred a worldwide trend over the past decade, inspiring a batch of BNPL companies, including several U.S. rivals such as Affirm, Block’s Afterpay and Sezzle.

An Affirm spokesperson declined to comment about when the Walmart partnership would conclude. In August, Affirm said in its quarterly shareholder letter that it expects to “substantially transition” from Walmart by its fiscal second quarter of 2026 as the retailer adds the exclusive tie to Klarna.

In May, Costco Wholesale said it would add Affirm as a BNPL option for sales of $500 or more made at its online store; although customers can also use Klarna through Apple’s digital wallet. Affirm has also been the primary BNPL option at Amazon since 2021 for purchases over $50 although that relationship is no longer exclusive.

London-based Klarna counts 790,000 merchants and 111 million consumers in 26 countries, the company said in August in releasing quarterly income results ahead of its initial public offering. The number of shoppers using the payment method jumped 31% for the second quarter, compared to the year-earlier period, the company said. The U.S. is the company’s largest market, according to its financial release.

For its long-awaited IPO, Klarna offered 34.3 million shares priced at $40. The company’s stock began trading Sept. 10 on the New York Stock Exchange.

Klarna views retail transactions as structured like a pyramid, with abundant lower-value purchases – tennis shoes, cosmetics and Uber – at the base and far fewer high-value transactions at the top, Sykes said. Klarna favors the higher volume approach.

“Some of our competitors start higher up on the pyramid,” he said. “They start with expensive electronics, expensive mattresses and all the rest. The challenge with that is there’s just less (purchasing) of them.”

The higher-end approach could have described U.S. rival Affirm in the past. At one point after the start of the COVID-19 pandemic, the maker of $1,000-plus Peloton stationary bikes was Affirm’s biggest client and accounted for a significant portion of its sales.

Despite its recent Walmart win supplanting Affirm, Sykes noted that retailers can offer multiple BNPL providers and said that attracting repeat users matters far more than snagging a spot on a retailer’s list of checkout options.

Target, for example, accepts payments from a half dozen BNPL providers including Klarna for online and mobile app purchases, while numerous retailers such as Best Buy, Macy’s and Dick’s Sporting Goods allow customers to use multiple BNPL providers for payment.

Klarna can be used for payment at dozens of merchants, including Airbnb, eBay, Foot Locker, Lowe’s and Neiman Marcus.

“I think we are totally agnostic as to whether a partner has one or multiple options, just to be totally frank,” Sykes said. Over the past 20 years, Klarna has learned that “it doesn’t matter what you do” beyond becoming the shopper’s first choice, he said.

“All that matters is consumer preference,” Sykes said. “Customers have to want to press that button. So when I think about where we spend most of our time and energy and effort, it’s giving the end consumer a heap of reasons to click that Klarna button.”

Article top image credit: Courtesy of Klarna Group

Digital payments to exceed $33.5 trillion by 2030

Consumers are predicted to rely less on their debit and credit cards and turn more to mobile wallets in the coming years, a Worldpay report predicts.

Payment provider Worldpay attributes the growth of digital wallet use in the U.S. to the COVID-19 pandemic. In the near future, digital wallets will play a more significant role in both e-commerce and point-of-sale payments and will be funded primarily by credit and debit cards, the report predicts.

Spending via digital payment methods, including digital wallets, buy now, pay later services and account-to-account payments, are predicted to surpass $33.5 trillion by 2030, according to the report. However, U.S. consumers use mobile wallets for only about four in ten (39%) of their online purchases and 16% of in-person transaction value, a smaller share than the 81% of e-commerce payments and 59% of point-of-sale transaction value in the Asia-Pacific region.

About two-thirds (67%) of all U.S. consumer purchases online and at points-of-sale were transacted via credit, debit and prepaid cards. Cash use in the U.S. fell from 44% of in-store spending in 2014 to 15% in 2024, the report found.

By 2030, digital wallets are expected to comprise more than half (52%) of e-commerce transaction value and 30% of point-of-sale transaction value, according to the report. By contrast, the report predicts that credit cards will comprise only 22% of e-commerce transaction value and 32% of point-of-sale purchases in 2030, down from 40% of online purchases and 48% of point-of-sale purchases in 2014.

As U.S. consumers increasingly adopt mobile wallets, cards remain a critical part of digital wallet usage in America and abroad. The report from Cincinnati, Ohio-based Worldpay notes that seven in ten digital wallets in the U.S. are funded by cards, tied with Australia (70%) and followed by the U.K. (67%), India (56%), Brazil (53%) and China (46%).

As for America’s attachment to cash, Worldpay’s report indicates that cash usage has been declining in the U.S. and will continue to drop in the coming years.

While a fifth of U.S. transaction value was cash-based in 2014, that share fell to 11% last year, according to Worldpay’s report. By 2030, U.S. consumers are predicted to use cash for only 9% of transaction value, per the report. Though the report categorized the U.S. as a medium-cash use country, other countries, such as Germany, Nigeria and Mexico, were categorized as high-cash use markets or low-cash use markets like South Korea, China, Sweden and Finland.

“A confluence of factors — advancements in smartphone technology, the exponential growth of fintech, and supportive regulatory frameworks — combined with changing consumer expectations for ease and convenience, have fundamentally transformed the way we make payments,” Adam Coyle, chief strategy officer at Worldpay, said in a statement.

Other reports illustrate Americans’ cash use. Last June, the Federal Reserve’s annual cash use survey found that about a third (32%) of consumers used credit cards for their payments, followed by 30% who used debit cards and 16% who used cash.

One possible driver of mobile wallet adoption in the U.S. is businesses integrating digital wallet capabilities. Large companies saw digital wallet usage spike from 48% in 2022 to almost two-thirds (64%) in 2023, according to a survey from the Federal Reserve’s financial services unit. Service businesses also saw their digital usage rise from 43% in 2022 to 61% in 2023, the survey found.

Another factor in the growing adoption of mobile wallets is the perception that they are more secure than other payment methods.

A 2023 J.D. Power survey found that the proportion of consumers who use digital wallets rose from 12% in 2022 to 48% in 2023. While the survey found that consumers under 40 have been using digital wallets due to perceived security, cybersecurity experts say that the payment method still carries vulnerabilities.

Because digital wallets can contain far more personal data than consumers’ card information, they are an even more enticing target for fraudsters, Sunny Thakkar, head of fraud and disputes at Worldpay, said.

Worldpay’s report also offered some insight into the dominant card issuers. Visa captured 63% of the card share in 2023, Mastercard was second at 25%, followed by American Express at 9%. Discover Financial Services— which is seeking to sell itself to Capital One for $35.3 billion — comprised only 1%, per the report. If approved, the larger Capital One could challenge Visa’s dominance.

Article top image credit: Permission granted by PDI Technologies

Google makes payments play

The search giant has locked arms with Wise, Klarna and others to improve and expand its payments services, including in remittances and e-commerce.

By: Patrick Cooley• Published Aug. 19, 2025

Search behemoth Google is deepening its relationship with companies like Wise, Affirm and Klarna as it seeks to make a broader payments play.

The tech titan said that it will incorporate remittance services into its digital wallet and buy now, pay later options into the autofill function in its signature Chrome web browser in a bid to make paying easier for shoppers.

Google said in a blog post that it will “soon” allow its Google Pay users to send cross-border payments through remittance providers like Ria Money Transfer, Xe and Wise.

Google will also let Chrome browser users add BNPL information to autofill for online purchases, the blog post said.

These moves are all about reducing friction in the payment process and ensuring more consumers complete transactions, according to consultants who follow the payments industry.

“Everything is about the path of least resistance,” Cliff Gray, principal at advisory firm Gray Consulting Ventures, said in an interview. “How many consumer purchases do companies lose because a person is on the site and they can’t find their wallet?”

Google’s announcement also came the same day that artificial intelligence start-up Perplexity made a long-shot offer to Google’s parent, Alphabet, to buy the Chrome web browser for $34.5 billion.

Chrome’s autofill lets users save their credit card information to avoid repeatedly entering the card numbers when making separate purchases. BNPL players Affirm and Zip are now autofill options and Klarna and Block-owned Afterpay are coming soon, the blog post said, although it did not provide a more precise timeline.

Google has already partnered with BNPL players in other ways. Afterpay and Klarna, for example, are among the options on Google Pay.

Klarna’s payment services will be added to Chrome’s autofill function later in 2025, the company said in its own news release. A spokesperson for Klarna said it would happen “in the coming months.”

A spokesperson for Block did not immediately respond to requests for further comment.

Google Pay users will at first be able to send remittances only to India, Brazil, Mexico and the Philippines, according to Google's blog post. Payments processing giant Stripe — which has a dual headquarters in Dublin, Ireland and San Francisco — will process the transactions, the blog post said.

A Google spokesperson did not immediately respond to a request for more details about the timeline or answer questions about how Google benefits financially from these arrangements.

Adding buy now, pay later options to autofill is another move to make the process of paying more seamless, said Mike Strawhecker, president of consulting firm The Strawhecker Group.

“Automatically showing BNPL options enhances utility, encouraging more users to complete purchases,” Strawhecker said in an email.

In addition, Google is almost certainly making these moves with OpenAI in mind, said Tony DeSanctis, senior director of payments for the consulting firm Cornerstone Advisors.

The artificial intelligence company is preparing to release its own web browser to compete with Google Chrome, and the search giant wants to give people more reasons to use its own product, he said in an interview.

“That’s why Google is adding all of these tools,” he said. “They need to make Chrome more valuable.”

Article top image credit: Brandon Bell via Getty Images

Retailers are pushing payment modernization as customers ask for more

A KPMG survey found that a majority of retailers plan to keep updating their payment programs to keep up with consumer tech demands.

By: Xanayra Marin-Lopez• Published March 6, 2025

As digital payments become more mainstream for consumers, retailers are trying to keep up with the payment methods they accept. Retailers need to make significant investments to navigate legacy systems, data security and privacy concerns, KPMG found.

Over half of retailers completed a major payments modernization program within the past year, a KPMG modernizing payments report found. For most retailers, the work is not over: 4 in 5 will once again update their payments infrastructure or plan to do so.

Almost 3 in 5 retailers in North America report changing customer expectations as the top factor triggering payment modernizations.

The findings are based on a survey by KPMG International of 810 financial institutions and 690 retailers.

A seamless payment experience is critical to customer satisfaction, according to a statement from Duleep Rodrigo, national sector leader of consumer and retail at KPMG U.S. The right delivery can improve operational efficiency and help provide insights into customer behavior, Rodrigo said.

When modernizing their payments, 3 in 5 retailers are working to upgrade and implement digital payments, KPMG found. Nearly the same number are working to add new payment options.

“Implementing and integrating new payments platforms can be complex and time-consuming,” Courtney Trimble, lead of global payments at KPMG, said in the report. “Despite these challenges, executives recognize the benefits of payment modernization as a catalyst for growth and innovation.”

One of the biggest roadblocks is cost. Nearly two-thirds of respondents said the top challenge when creating a modern payments program for retail is the cost of implementing new technologies. For over half of respondents, training staff from old to new systems is also a challenge.

Rodrigo said that younger generations of consumers increasingly gravitate to contactless payments, mobile wallets and other digital solutions compared to cash and credit cards. In support of digital efforts, three-fifths of retailers surveyed already offer an app or plan to launch one.

Though Gen Z in particular enjoys in-person shopping, their preferred methods of payment lean digital.

However, frictionless payments come with its pros and cons. While contactless methods of paying can cut transaction times, improve data security and boost customer satisfaction, they are still more vulnerable to certain privacy risks. Bad actors can exploit consumer behavior information for purposes like unauthorized purchases.

Article top image credit: Getty Images

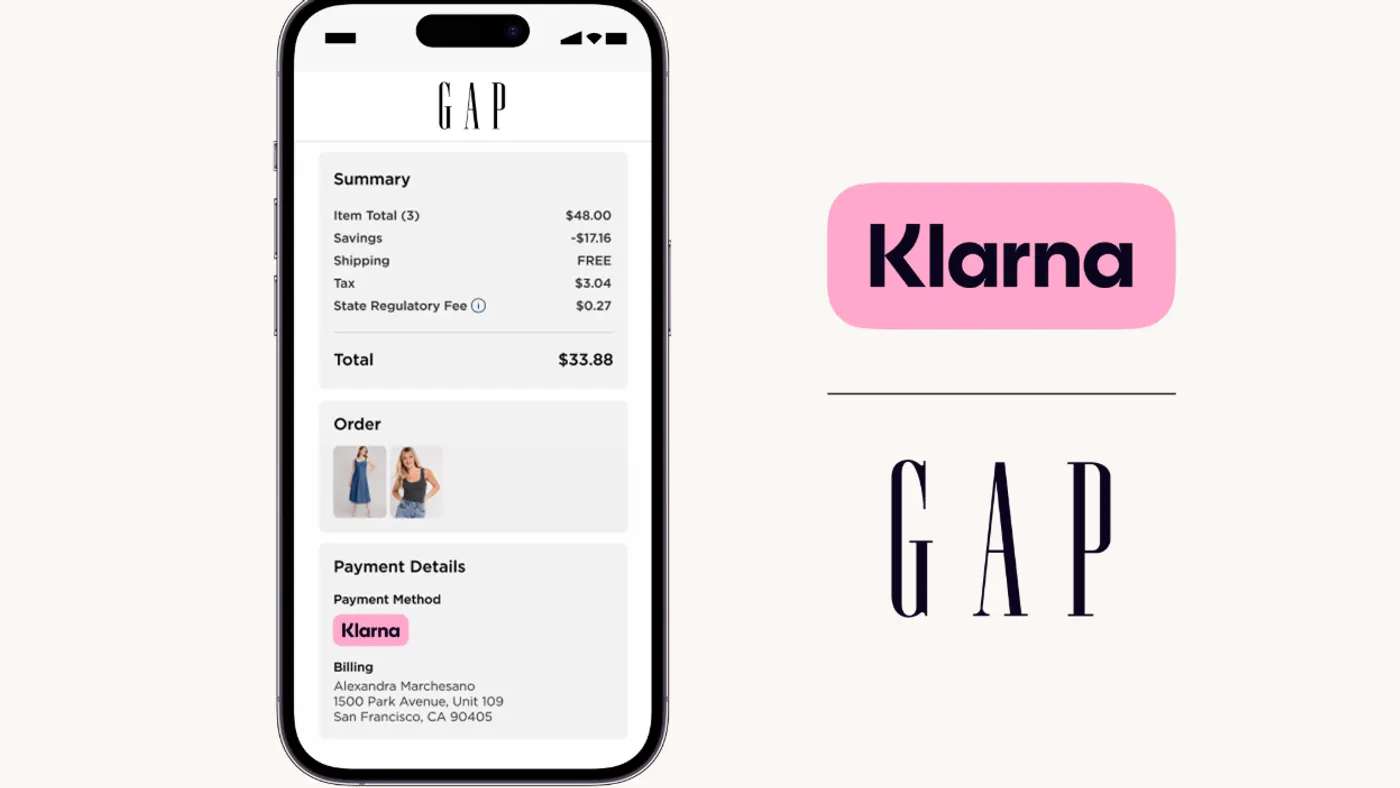

Gap Inc. teams up with Klarna on flexible payments

The apparel retailer is offering Klarna’s payment services to U.S. shoppers across its portfolio of brands, including Old Navy and Athleta.

By: Tatiana Walk-Morris• Published Sept. 18, 2025

Gap Inc. wants to give shoppers different ways to pay. The apparel company has partnered with Klarna to offer the payment provider’s services across its portfolio of brands including Old Navy, Gap, Banana Republic and Athleta.

With Klarna, U.S. customers can pay for their Gap Inc. purchases in full or in four interest-free installments online or within the mobile app, according to a press release. The Gap Inc. partnership adds to Klarna’s growing customer base, which has surpassed 26 million U.S. shoppers and 724,000 sellers worldwide.

Other than the company teaming up with Klarna, the apparel retailer also allows customers to purchase items through Apple Pay and Afterpay, among other options.

"We are excited to offer our customers more choice, convenience and control by offering a variety of payment options across our portfolio of brands," Kevin Meiners, head of loyalty and payments at Gap Inc., said in a statement.

Gap Inc.’s partnership with Klarna comes as the company seeks to attract customers amid a turnaround. The company’s namesake brand recently unveiled its global fall 2025 campaign, which highlights its low-rise denim collection and stars girl group Katseye. Drawing inspiration from the early 2000s, Gap’s 90-second ad features singer Kelis’ hit song “Milkshake” and has largely been met with positive reviews.

Shortly after that campaign launch, Gap Inc. reported flat Q2 net sales and a 1% increase in comps compared to last year. Inventory increased 9% year over year, which the company attributed to tariffs and its effort to import products before duties increased.

In addition to announcing its partnership with Gap Inc., Klarna will begin to offer its short-term loans at Walmart later in September.

As Klarna adds more retail partners to its growing roster, research suggests that consumers, particularly younger shoppers, are turning to buy now, pay later providers as an alternative to credit cards.

Article top image credit: Courtesy of Klarna

Third of US small businesses add credit card surcharges

The findings of a J.D. Power survey indicate that merchants are passing the cost of swipe fees onto customers, even though they’re lowering consumer satisfaction with the transaction.

By: Patrick Cooley• Published Feb. 3, 2025

A third of small businesses in the U.S. are now adding surcharges to credit card transactions, according to a recent J.D. Power survey.

The data analytics firm surveyed 3,841 U.S. small businesses and found that 34% said they added a surcharge when a customer paid with a card. This was the first J.D. Power survey that included a question about surcharges and credit cards.

The results of the annual survey carry possible implications for credit card networks, said John Cabell, managing director of payments intelligence for J.D. Power.

Card networks charge merchants interchange fees — also called swipe fees — on credit card transactions. Those fees typically amount to between 2% and 4% of the total value of the transaction, according to the National Retail Federation.

“A lot of consumers are saying that [surcharges] are influencing their payment decision,” Cabell said.

Financial advice website LendingTree surveyed 1,555 credit card holders in August 2023 and found that 73% said they would use credit cards less if they had to regularly pay surcharges when they use those cards.

Consumer satisfaction was also marginally lower for merchants that assessed these surcharges, J.D. Power found in its survey, which was released Jan. 14. Satisfaction rates were 24 points lower (on a 1,000 point scale) for businesses that add credit card surcharges to a customer’s bill, compared with those that don’t, the survey found.

“The 24 point difference in cost of processing satisfaction is based on scores of 628 for those merchants who levy surcharges and 652 for those merchants who do not,” a J.D. Power spokesperson said in an email.

While the data firm did not ask about surcharges in previous surveys, Cabell said the extra costs do seem to have become more prevalent recently.

“We have seen in the last few years service fees and convenience fees crop up at various types of businesses,” he said. “I think that merchants increasingly are passing on costs to consumers in a more explicit fashion.”

Interchange fees became a political lightning rod in recent years as state and federal lawmakers put credit card networks in the spotlight over whether the extra costs charged to merchants should be permitted or not.

State legislatures, for example, have passed laws limiting such fees. One of those states is Illinois, which sparked controversy when it passed a law saying that the fees couldn’t be imposed on taxes and tips.

Congressional panels have also grilled card network executives over the fees, suggesting that Visa and Mastercard have a monopoly in the market that allows them to charge excessive fees.

Banks that issue the cards and the major card networks are fighting back.

A U.S. District Court judge partially halted the Illinois law that would have barred interchange fees on taxes and tips after a coalition of groups that represent banks and credit card networks — including the American Bankers Association — challenged it.

Judge Virginia Kendall imposed a partial preliminary injunction in December that said the law applied to state banks and credit unions, but prevented the state from applying it to national banks and federal savings associations.

Article top image credit: Getty Images

Klarna to displace Affirm as Walmart BNPL provider

The Swedish buy now, pay later business partnered with a Walmart-backed fintech to offer loans at the retail giant via a digital payments app.

Those installment loans will be offered through OnePay, a digital payments app that Walmart shoppers can use at checkout online and in the store, Klarna said in a news release. OnePay is a service provided by One, the fintech established by Walmart and venture capital firm Ribbit Capital in 2021 that is majority owned by the retailer.

The change will be made gradually, a Klarna spokesperson said in an email. OnePay will start integrating Klarna installment loan options into Walmart’s checkout in the coming weeks and those options “will be scaled to all Walmart channels by the holiday season,” the spokesperson said.

Klarna products available to Walmart customers include loans ranging from three months to 36 months, the spokesperson said.

The move gives Klarna access to a Walmart customer base that spends hundreds of billions of dollars every year. Walmart is the largest retailer in the United States, based on 2023 sales according to the National Retail Federation. Walmart reported $681 billion in revenue for the fiscal year that ended on Jan. 31, according to an earnings report.

“We will continue our long-term strategy of competing on our products and entering into sustainable partnerships,” an Affirm spokesperson said in an emailed statement that did not address the Walmart news.

Affirm installment loans are still available as an option at Walmart’s checkout at this point, the company said in an SEC filing. The BNPL provider noted that sales through Walmart were about 5% of its gross merchandise volume for the second half of last year. They also represented about 2% of its adjusted operating income.

“Although the loss of a significant retail partner, especially one as important as Walmart, is impossible to spin positively, in our opinion, there is a key reason why Klarna’s reported contract is not one that Affirm would favor,” William Blair analysts wrote in a note to investors.

Affirm prefers to control the user experience, and would not have wanted to cede control over that experience to OnePay, the analysts wrote.

Article top image credit: Kaarin Vembar/Retail Dive

Stitch Fix adds Affirm’s buy now, pay later services at checkout

The option will give customers “flexibility and control” over their purchases, as the company continues to bolster services.

At checkout, Stitch Fix shoppers will go through a real-time eligibility check. If approved, shoppers can stretch their purchases across monthly payments without late fees, the company said.

The service is now available on Stitch Fix’s website and mobile app. Stitch Fix’s new Affirm integration follows the company’s efforts to add new features and bolster its business.

“Stitch Fix’s personal styling service has long been known for helping its clients discover the styles they love, and we’re excited to work with Stitch Fix to offer those clients more flexibility and control over how they pay for their purchases,” Pat Suh, senior vice president of revenue at Affirm, said in a statement.

In addition to adding a new payment option for customers, Stitch Fix has been highlighting its stylist talent. Last year, the companybegan testing stylist profiles with information about their interests, work portfolios and expertise. Then it introduced the feature incrementally with more details about their stylists, such as fun facts, client testimonials and specialties.

In its Q1 earnings, the companyreported a 12.6% decline in net revenue year over year to $318.8 million. Stitch Fix also said its number of active clients dropped 18.6% from the previous year. However, its net losses narrowed from $35.5 million in the year-ago period to $6.2 million.

“Our clients are responding to the newness we have brought to our assortment as well as the improvements we’ve made to our client experience,” Baer said in a statement at the time. “This progress is a testament to the Stitch Fix team’s ongoing execution of our transformation strategy, and we continue to expect to return to revenue growth by the end of FY26.”

Article top image credit: Courtesy of Stitch Fix

The biggest payment trends in retail

Retailers are thinking through the best way to streamline and incorporate payment options as a way to capture, delight and retain shoppers. Millennial and Gen Z shoppers are leading the way when it comes to contactless payment adoption, and retailers are rolling out options like buy now, pay later and checkout-free capabilities.

included in this trendline

ChatGPT lets shoppers buy products within the platform

Checkout-free payments may yet rise

Gap Inc. teams up with Klarna on flexible payments

Our Trendlines go deep on the biggest trends. These special reports, produced by our team of award-winning journalists, help business leaders understand how their industries are changing.